Politically Exposed Person (PEP): Meaning, Risks, and Compliance Requirements

Wahat Is a Politically Exposed Person?

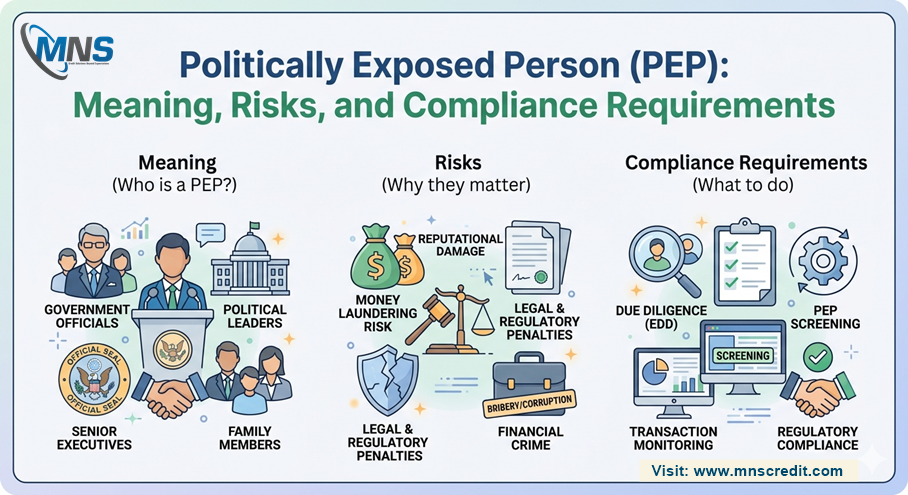

A Politically Exposed Person, commonly referred to as a PEP, is an individual who holds or has recently held a prominent public position — one that carries significant influence over governmental, judicial, military, or state-controlled commercial functions. The Financial Action Task Force (FATF), the global standard-setter for anti-money laundering and counter-terrorism financing, defines PEPs as individuals who have been entrusted with prominent public functions, either domestically or in foreign jurisdictions.

The PEP category encompasses a wide range of individuals. Domestic PEPs include heads of state and government, senior politicians and members of parliament, senior judicial officials, high-ranking military officers, senior executives of state-owned enterprises, and senior officials of central banks and major regulatory bodies. Foreign PEPs are equivalent individuals from other countries. International organisation PEPs include senior officials of international bodies such as the United Nations, World Bank, International Monetary Fund, and regional development banks.

The definition also extends to close associates and family members — spouses, children, parents, siblings, and known business associates — who may be used as proxies to conceal a PEP's beneficial interest in assets or transactions. This extended definition reflects the reality that financial crime involving PEPs frequently operates through family members and associates who have fewer formal restrictions placed upon them.

Why PEPs Represent Elevated Financial Crime Risk

The PEP classification exists because individuals who hold or have held significant public positions are statistically more exposed to involvement in bribery, corruption, and the misuse of public funds than the general population. Their positions of authority create both the opportunity and the potential motive for financial misconduct — and the financial flows that result from such misconduct must be concealed and integrated into the legitimate financial system through money laundering.

The risk is not that every PEP is corrupt — the vast majority are not. The risk is that a proportion of individuals in PEP-qualifying positions do misuse their authority, and the financial transactions associated with such misuse are specifically designed to appear legitimate. Without enhanced scrutiny of PEP-related transactions, financial institutions and other regulated businesses become unwitting vehicles for the concealment of proceeds from corruption, bribery, and misappropriation of public assets.

Historical cases of PEP-related financial crime have involved state funds diverted through complex corporate structures, real estate purchases funded by unexplained wealth, investment products used to layer corrupt proceeds, and family members used to distance the PEP from the beneficial ownership of assets. These cases underscore why the enhanced due diligence framework applied to PEPs is not bureaucratic excess — it is a proportionate response to demonstrated patterns of risk.

Regulatory Requirements: Enhanced Due Diligence for PEPs

In India, the Prevention of Money Laundering Act (PMLA) and the guidelines issued by the Reserve Bank of India, SEBI, IRDAI, and other regulators impose specific obligations on financial institutions and other reporting entities when dealing with PEPs. These obligations reflect the FATF Recommendations and are broadly consistent with global compliance practice, though the specific application varies by sector and institution type.

Customer identification and verification requirements for PEPs go beyond standard KYC procedures. Institutions must obtain senior management approval before establishing or continuing a business relationship with a PEP, must implement enhanced ongoing monitoring of all transactions involving PEP relationships, and must take reasonable measures to establish the source of wealth and source of funds associated with a PEP customer or transaction.

The requirement to establish source of wealth — how the PEP accumulated their overall wealth — is particularly significant. A senior government official with a declared salary of Rs. 10 lakh per annum who is investing Rs. 5 crore in financial products cannot satisfy source of wealth requirements by simply referencing their salary. Enhanced due diligence must probe whether the claimed source of wealth — inheritance, prior business activity, investment returns — is plausible and consistent with the documented evidence available.

PEP Screening: Identifying PEPs in the Customer Base

The first practical challenge of PEP compliance is identification — determining which customers or counterparties in a financial institution's existing or prospective customer base qualify as PEPs or PEP associates. PEP screening involves checking customer names against commercially maintained PEP databases that compile information on individuals who hold or have held qualifying public positions, their immediate family members, and their known associates.

Effective PEP screening must address several practical challenges. Name matching across different transliterations and scripts requires sophisticated fuzzy matching algorithms that go beyond exact name comparison. PEP status is dynamic — individuals enter and exit qualifying positions, and former PEPs typically remain subject to enhanced scrutiny for a defined period (commonly 12 to 24 months) after leaving their position. And the international dimension of PEP screening requires access to databases that cover foreign PEPs across all relevant jurisdictions, not merely domestic political figures.

Ongoing Monitoring and Transaction Surveillance

For financial institutions with existing PEP customers, enhanced ongoing monitoring is a continuous compliance obligation. Transactions involving PEP accounts must be subject to heightened scrutiny for patterns that are inconsistent with the customer's known business, income, and risk profile. Large cash transactions, complex multi-step fund transfers, sudden changes in transaction patterns, and transactions involving jurisdictions with high corruption risk all warrant closer examination in PEP accounts than in standard customer accounts.

The practical implementation of enhanced PEP monitoring requires transaction monitoring systems that are calibrated to flag the specific risk patterns associated with PEP financial crime — systems that apply more sensitive thresholds and more sophisticated pattern recognition to PEP accounts than to the general customer population. Firms that apply the same monitoring parameters to PEP accounts as to standard customers are not meeting their enhanced due diligence obligations in substance, even if they are meeting them in form.

Conclusion

PEP compliance is one of the most demanding and consequential elements of an AML framework — demanding because of the complexity of PEP identification, enhanced due diligence execution, and ongoing monitoring; consequential because the regulatory, reputational, and financial costs of getting it wrong are severe. Financial institutions and other regulated businesses that invest in building genuinely robust PEP compliance programmes — comprehensive screening, rigorous enhanced due diligence, senior management oversight, and calibrated transaction monitoring — are managing one of the most significant financial crime risks in their customer base with the seriousness it deserves.