How Inflation Can Impact Your Retirement Savings

Retirement planning requires consistent effort, and working with an Investment Advisor Dubai professional can help individuals prepare for financial challenges that develop over time, including inflation. While many people focus on saving enough money for retirement, they often overlook how rising prices gradually reduce the purchasing power of those savings. Inflation may appear manageable in the short term, but over several decades, it can significantly affect the lifestyle retirees expect to enjoy. Understanding how inflation works and planning for its long-term effects can help individuals build a retirement strategy that remains effective despite changing economic conditions.

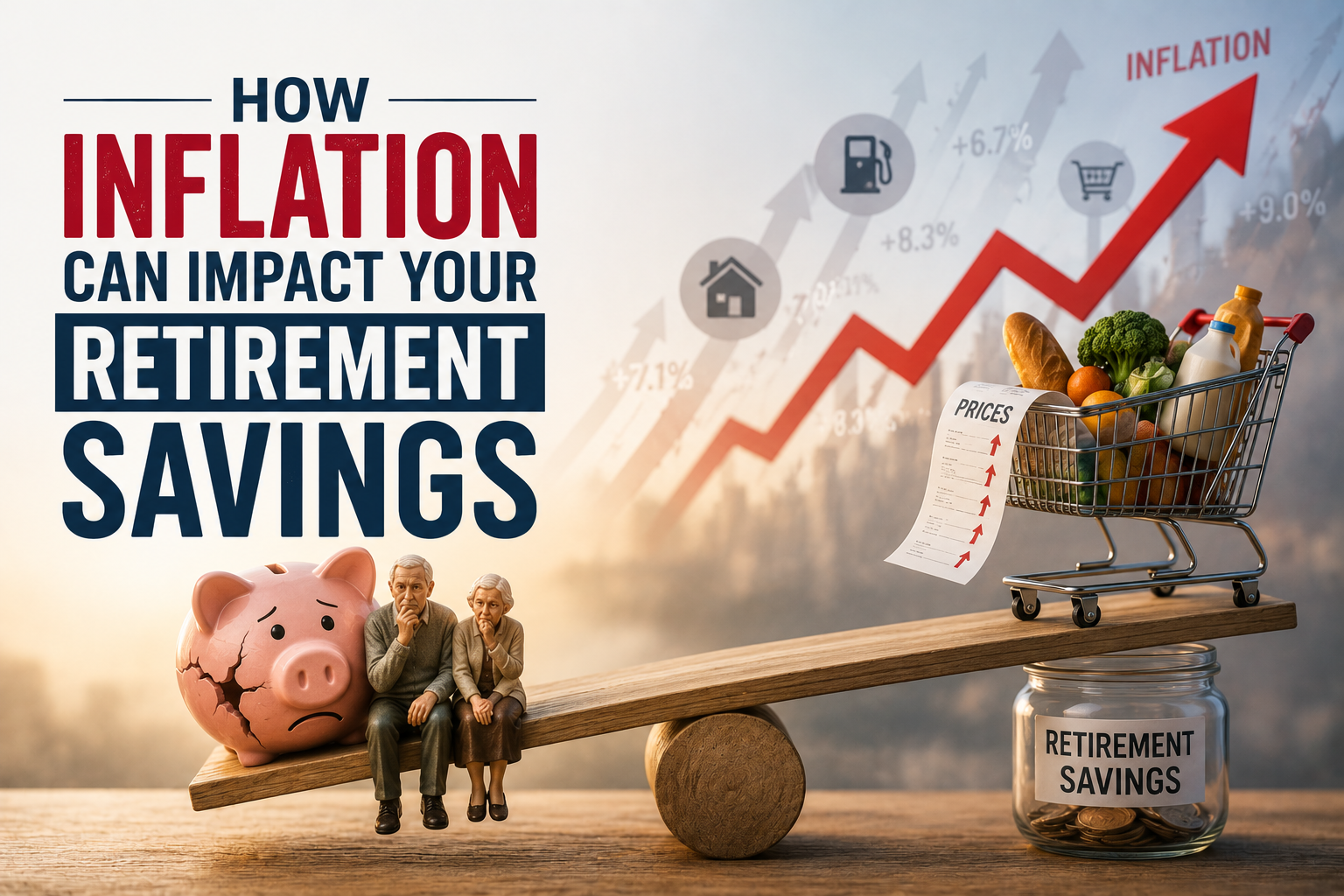

Understanding Inflation and Its Long-Term Effects

Inflation refers to the gradual increase in the prices of goods and services over time. As prices rise, each unit of currency buys fewer products than it did before. Even a relatively low annual inflation rate can have a substantial impact over twenty or thirty years. For retirees who depend on accumulated savings, this means the same amount of money will likely cover fewer expenses in the future.

Many everyday costs, including housing, transportation, groceries, utilities, and healthcare, tend to increase over time. Without proper planning, retirement income that appears sufficient today may become inadequate years later. This makes inflation one of the most important factors to consider when developing a long-term financial strategy.

Why Retirement Savings Need to Outpace Inflation

Simply saving money is not always enough. If retirement savings grow at a rate lower than inflation, the real value of those funds gradually declines. For example, money sitting in a low-interest savings account may appear safe, but if inflation consistently exceeds the earned interest, purchasing power decreases year after year.

Successful retirement planning focuses on growing assets in a way that helps offset inflation. This usually involves maintaining a diversified investment strategy that balances growth opportunities with acceptable levels of risk. The objective is not only to preserve capital but also to increase its value over the long term.

The Compounding Effect of Inflation

One reason inflation becomes so significant is because it compounds over time. Just as investments can benefit from compound returns, inflation compounds by increasing the cost of living each year based on already higher prices.

Consider someone planning to retire in twenty-five years. An annual expense that seems manageable today may cost considerably more by the time retirement begins. Likewise, healthcare costs, insurance premiums, and home maintenance expenses often rise faster than the average inflation rate, placing additional pressure on retirement budgets.

Understanding this compounding effect encourages individuals to estimate future expenses rather than relying solely on today's prices when calculating retirement needs.

Healthcare Costs Often Rise Faster

Healthcare represents one of the largest expenses during retirement, and it frequently experiences inflation at a higher rate than many other consumer goods. Medical treatments, prescription medications, specialist consultations, and long-term care services often become more expensive over time.

Longer life expectancy also means retirees may require healthcare support for many years. Without sufficient financial preparation, rising medical costs can significantly reduce retirement savings. Including healthcare inflation in retirement projections helps create a more realistic financial plan that accounts for future needs rather than current expenses alone.

The Importance of Investment Growth

Investments play a key role in helping retirement savings maintain their purchasing power. While every investment carries some level of risk, avoiding growth-oriented investments entirely may expose retirement savings to inflation risk instead.

Diversification allows investors to spread assets across different investment categories, helping reduce reliance on a single source of returns. Depending on individual goals, risk tolerance, and retirement timeline, a balanced portfolio may include equities, fixed-income investments, real estate, and other suitable financial instruments.

Regular portfolio reviews help ensure investments continue supporting long-term objectives while adapting to changing economic conditions.

Adjusting Retirement Contributions Over Time

Many people begin retirement planning by selecting a monthly savings target and continuing that amount for years. However, inflation affects not only future expenses but also the amount that should be saved throughout a career.

Increasing retirement contributions whenever income rises can help maintain progress toward financial goals. Annual adjustments, even if relatively small, can significantly improve retirement outcomes over several decades. Salary increases, bonuses, and reduced debt obligations provide opportunities to increase retirement savings without dramatically affecting current lifestyles.

Consistently reviewing contribution levels allows retirement plans to remain aligned with future purchasing power rather than today's economic conditions.

Income Planning During Retirement

Retirement planning extends beyond accumulating savings. Developing a sustainable income strategy becomes equally important after retirement begins. Withdrawals that appear manageable initially may become insufficient if living expenses continue increasing due to inflation.

A carefully structured withdrawal strategy considers expected investment growth, anticipated inflation, life expectancy, and changing spending patterns. Maintaining flexibility allows retirees to adjust withdrawals as economic conditions evolve while helping preserve retirement assets for a longer period.

Planning income sources carefully can reduce the likelihood of exhausting retirement savings prematurely.

Diversification Reduces Long-Term Risk

Inflation affects different asset classes in different ways. Some investments may perform better during inflationary periods, while others may struggle. Maintaining diversification helps reduce the impact of economic uncertainty by avoiding excessive dependence on a single investment type.

Diversification should also evolve throughout different life stages. Younger investors often have more time to recover from market fluctuations, allowing greater exposure to growth-oriented investments. As retirement approaches, portfolios typically become more balanced to protect accumulated wealth while still providing opportunities for continued growth.

Regular adjustments help ensure investment allocations remain appropriate for changing financial objectives.

Reviewing Retirement Plans Regularly

Retirement planning should never become a one-time exercise. Inflation rates, investment performance, tax regulations, income levels, and personal financial goals all change over time. Periodic reviews help identify whether current savings remain sufficient to meet future retirement needs.

Life events such as marriage, career changes, business ownership, inheritance, or major purchases may also require adjustments to retirement strategies. Reviewing plans annually allows individuals to make gradual improvements rather than major corrections later in life.

Consistent monitoring provides greater confidence that retirement objectives remain achievable despite changing economic conditions.

Building Financial Confidence for the Future

Inflation cannot be eliminated, but its impact can be managed through thoughtful financial planning. Individuals who understand the relationship between inflation, investment growth, and retirement income are generally better prepared to protect their long-term financial security.

Starting early provides a significant advantage because longer investment horizons allow savings to benefit from compound growth while giving investors time to navigate market fluctuations. Even those beginning retirement planning later can improve outcomes through disciplined saving, realistic expectations, and regular financial reviews.

Financial education remains one of the strongest tools for making informed retirement decisions. Understanding how inflation influences future purchasing power encourages proactive planning rather than reactive decision-making.

Conclusion

Preparing for retirement involves much more than reaching a savings target. Inflation continuously changes the cost of living, making it essential to build a retirement strategy that accounts for future purchasing power instead of present-day expenses. By increasing savings consistently, maintaining diversified investments, reviewing financial plans regularly, and adapting to economic changes, individuals can better protect their retirement lifestyle against inflation over the long term. Making informed decisions today creates a stronger financial foundation for tomorrow, especially when long-term guidance is supported by a qualified Financial Advisor in Dubai who understands evolving retirement planning needs.