Rapid Prototyping Service Market Revenue Forecast and Business Opportunities Through 2034

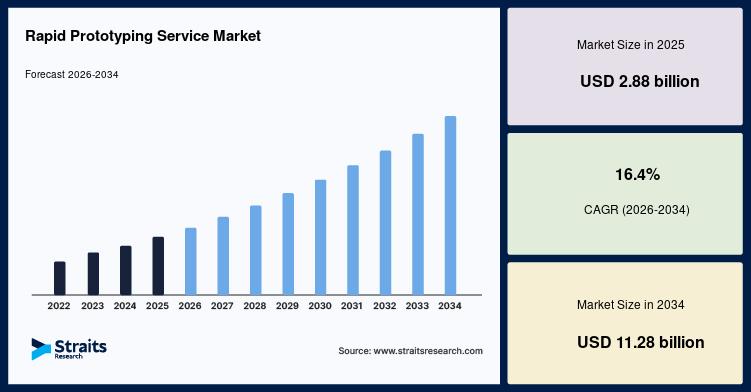

The global rapid prototyping service market is witnessing remarkable growth due to increasing adoption of additive manufacturing technologies, rising demand for faster product development cycles, and growing investments in digital manufacturing across industries. The global rapid prototyping service market size was valued at USD 2.88 billion in 2025 and is projected to grow from USD 3.35 billion in 2026 to USD 11.28 billion by 2034, registering a CAGR of 16.4% during the forecast period (2026–2034).

Rapid prototyping services enable manufacturers to quickly design, test, and validate product concepts using advanced technologies such as 3D printing, computer-aided design (CAD), and additive manufacturing. These services significantly reduce product development time, improve design flexibility, lower production costs, and accelerate time-to-market. Increasing demand for customized products, continuous innovation in manufacturing technologies, and the growing adoption of Industry 4.0 are expected to drive market expansion throughout the forecast period.

Market Drivers

One of the primary factors driving the rapid prototyping service market is the increasing adoption of additive manufacturing technologies. Industries such as automotive, aerospace, healthcare, consumer electronics, and industrial manufacturing are increasingly utilizing rapid prototyping services to accelerate product development and improve design accuracy. The ability to produce complex prototypes with minimal material waste makes these services highly attractive for manufacturers.

Another significant growth driver is the growing need to shorten product development cycles. Companies are under constant pressure to launch innovative products faster while reducing development costs. Rapid prototyping enables businesses to evaluate multiple design iterations, identify defects early, and make modifications before mass production, resulting in improved product quality and reduced time-to-market.

The expanding use of rapid prototyping in the healthcare sector is also contributing to market growth. Medical device manufacturers are increasingly using rapid prototyping services to develop customized implants, surgical guides, prosthetics, dental devices, and anatomical models. Advances in 3D printing technologies continue to expand applications in personalized healthcare.

Furthermore, increasing investments in Industry 4.0, digital manufacturing, and smart factories are creating new growth opportunities. The integration of artificial intelligence, cloud computing, simulation software, and digital design tools is enhancing prototype development while improving manufacturing efficiency and product innovation.

Market Challenges

Despite strong growth prospects, the rapid prototyping service market faces several challenges.

One of the major restraints is the high cost of advanced rapid prototyping equipment and materials. Sophisticated 3D printers, specialized materials, and software solutions require significant capital investment, which may limit adoption among small and medium-sized enterprises.

Another challenge is the shortage of skilled professionals capable of designing, operating, and optimizing advanced rapid prototyping technologies. Organizations require experienced engineers and technical specialists to maximize the benefits of additive manufacturing.

Additionally, material limitations and quality consistency remain challenges for certain industrial applications. Manufacturers continue investing in research to develop stronger, lighter, and more durable materials suitable for production-grade prototypes and end-use components.

Market Segmentation

By Technology

- Stereolithography (SLA)

- Selective Laser Sintering (SLS)

- Fused Deposition Modeling (FDM)

- PolyJet Printing

- Others

The fused deposition modeling (FDM) segment accounts for the largest market share owing to its cost-effectiveness, ease of use, and widespread adoption across automotive, aerospace, consumer goods, and educational applications. Its ability to rapidly produce functional prototypes continues to drive segment growth.

By Application

- Automotive

- Aerospace and Defense

- Healthcare

- Consumer Electronics

- Industrial Manufacturing

- Others

The automotive segment dominates the market due to increasing demand for rapid design validation, functional testing, and lightweight component development. Automotive manufacturers rely on rapid prototyping services to accelerate product innovation while reducing production costs.

By End User

- Large Enterprises

- Small and Medium Enterprises (SMEs)

The large enterprises segment holds the largest market share owing to significant investments in advanced manufacturing technologies, product innovation, and digital transformation initiatives. However, SMEs are increasingly adopting rapid prototyping services to improve competitiveness and reduce product development timelines.

Regional Insights

North America

North America dominates the global rapid prototyping service market due to its advanced manufacturing infrastructure, strong adoption of additive manufacturing technologies, and the presence of leading aerospace, automotive, and healthcare companies. The United States continues to drive regional growth through significant investments in digital manufacturing and product innovation.

Europe

Europe represents a significant market supported by increasing adoption of Industry 4.0 technologies, expanding automotive and aerospace industries, and strong investments in research and development. Growing emphasis on advanced manufacturing and sustainable production continues to strengthen regional market growth.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period owing to rapid industrialization, expanding manufacturing capabilities, increasing adoption of 3D printing technologies, and rising investments in smart manufacturing across China, India, Japan, South Korea, and Southeast Asian countries.

Latin America, Middle East, and Africa

These regions are emerging markets driven by growing industrial development, increasing investments in manufacturing modernization, expanding aerospace and automotive sectors, and rising awareness regarding advanced prototyping technologies.

Key Players Analysis

The rapid prototyping service market is highly competitive, with leading companies focusing on advanced additive manufacturing technologies, material innovation, strategic partnerships, and expansion of digital manufacturing capabilities. Continuous investments in research and development are enabling companies to deliver faster, more accurate, and cost-effective prototyping solutions across multiple industries.

Major companies operating in the market include:

- Protolabs, Inc.

- Materialise NV

- Stratasys Ltd.

- 3D Systems Corporation

- EOS GmbH

- Sculpteo

- Xometry, Inc.

- ProtoCAM

- Fast Radius, Inc.

- Renishaw plc

These companies continue expanding their service portfolios, investing in next-generation additive manufacturing technologies, and strengthening global production networks to meet the growing demand for rapid prototyping services across industrial sectors.

For Detailed Insights, Visit:

https://straitsresearch.com/report/rapid-prototyping-service-market

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: sales@straitsresearch.com

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)